In recent years, the financial landscape has transformed significantly with the advent of digital technology. One of the most prominent changes is the rise of online loan approval processes, allowing borrowers to apply for and get loans sanctioned without ever stepping foot in a bank or lending institution. But the question remains: Is online loan approval right for you?

This article dives deep into the mechanics of online loan approval, its advantages and disadvantages, the eligibility criteria, and the factors you should consider before opting for an online loan. By the end, you will have a clearer understanding of whether this modern borrowing method aligns with your financial needs and circumstances.

Key Takeaways

- Online loan approval speeds up borrowing by leveraging digital technology.

- It offers convenience and accessibility but requires careful lender selection.

- Interest rates and fees vary; compare multiple options before applying.

- Suitable for emergency funds, tech-savvy borrowers, and those without easy bank access.

- Not ideal for those needing personalized support or with poor credit.

- Always prioritize data security and lender credibility.

- Timely repayment is crucial to maintain financial health and creditworthiness.

Understanding Online Loan Approval

In today’s digital age, financial services have embraced technology to simplify and accelerate processes that once took weeks or even months. One such process is loan approval, which has been revolutionized by the concept of online loan approval. But what exactly does this term mean, and how does it work?

What Is Online Loan Approval?

Online loan approval refers to the entire process of applying for and getting a loan sanctioned through internet-based platforms, without the need for physical paperwork or visiting a bank branch. Borrowers can submit their loan applications via websites or mobile apps, upload necessary documents digitally, and receive approval notifications electronically.

This digital transformation has made borrowing more accessible, faster, and more convenient for millions of people worldwide.

How Does Online Loan Approval Work?

The traditional loan approval process involved multiple steps — filling out forms manually, submitting physical documents, waiting for manual verification, and often visiting the lender’s office. In contrast, online loan approval leverages automation and digital tools to streamline these steps:

- Application Submission:

The borrower visits the lender’s website or app and fills out an online application form. This form typically requires personal details (name, address, date of birth), financial information (income, employment status), and loan specifics (amount requested, tenure). - Document Upload:

Instead of physical copies, borrowers upload scanned or photographed versions of required documents such as identity proof, income statements, bank statements, and sometimes address proof. Many platforms support instant document upload through smartphones. - Automated Credit Assessment:

Once the application and documents are submitted, the lender’s backend system automatically checks the borrower’s creditworthiness. This involves analyzing credit scores, repayment history, existing debts, and other financial factors. Advanced algorithms and artificial intelligence may be used for faster and more accurate assessment. - Instant or Quick Decision:

Based on the automated evaluation, the system generates an instant or near-instant loan approval decision. If approved, the borrower receives a notification via email, SMS, or within the app. - Loan Agreement and Disbursal:

The borrower can review and digitally sign the loan agreement online. After acceptance, the loan amount is disbursed directly to the borrower’s bank account, often within a few hours or the same day.

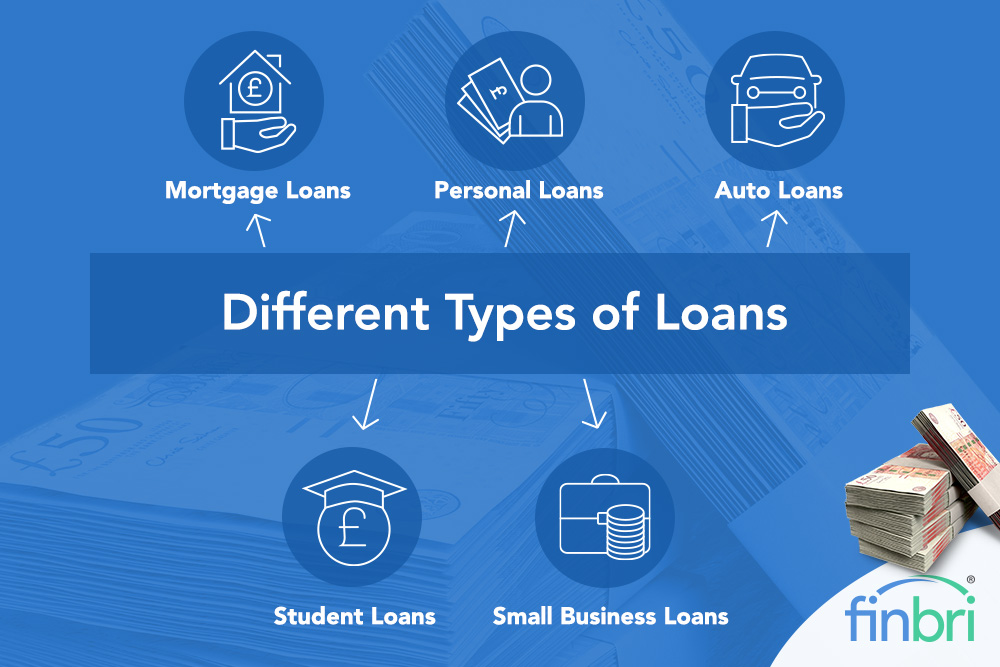

Types of Loans Available Through Online Loan Approval

he landscape of lending has evolved significantly with digital innovation, making various types of loans accessible through online platforms. Online loan approval is no longer limited to just personal or payday loans; today, a wide spectrum of loan products can be applied for and approved entirely online. Understanding the different types of loans available helps borrowers choose the right product tailored to their specific financial needs.

Personal Loans

Personal loans are among the most popular loan types available via online loan approval. These are unsecured loans, meaning you don’t need to provide collateral like a house or car. Borrowers can use personal loans for a variety of purposes — from consolidating debt and financing a wedding to covering emergency expenses or even vacation costs.

Online personal loans typically have flexible repayment terms ranging from a few months to several years, with fixed or variable interest rates. Because they are unsecured, interest rates can be higher compared to secured loans, but the convenience and quick approval often outweigh the costs.

Payday Loans

Payday loans are short-term, small-dollar loans designed to cover urgent cash needs until the borrower’s next paycheck. They are often available through online loan approval platforms due to the urgency they serve.

While payday loans provide rapid funding, sometimes within hours, they usually come with high interest rates and fees. Therefore, they are best suited for borrowers who can repay quickly and avoid long-term debt traps.

Home Loans (Mortgages)

Online loan approval has expanded into the home loan market, enabling borrowers to apply for mortgages digitally. Many traditional banks and newer fintech lenders offer online application processes for home purchase loans, refinancing, or home equity loans.

The online process for home loans involves uploading detailed documentation like income proofs, credit reports, and property documents. Though approval for home loans takes longer than personal loans, the online platforms significantly reduce paperwork and accelerate pre-approval stages.

Auto Loans

Buying a vehicle often requires financing, and online loan approval makes it easier to obtain auto loans quickly. Borrowers can compare rates, loan tenures, and EMI options from multiple lenders in one place before applying.

Online auto loans can be either secured (where the vehicle serves as collateral) or unsecured, depending on the lender’s terms. Digital approvals often include instant credit checks and document verification, speeding up vehicle purchase financing.

Business Loans

Small and medium enterprises (SMEs) and startups increasingly rely on online loan approval platforms to secure business loans. These loans can fund expansion, inventory purchases, equipment upgrades, or working capital needs.

Online business loans typically require financial documents like business registration certificates, income statements, and bank statements. Some lenders use alternative data (like cash flow and transaction history) for credit evaluation, making loans accessible even to newer businesses.

Student Loans

Education financing is another domain where online loan approval plays a crucial role. Students and parents can apply for student loans to cover tuition fees, accommodation, books, and other expenses.

Many online student loan providers offer competitive interest rates and flexible repayment options, sometimes with grace periods until after graduation. The online application process simplifies accessing funds quickly, especially for international or distance learners.

Debt Consolidation Loans

Debt consolidation loans allow borrowers to combine multiple existing debts — like credit cards, medical bills, or personal loans — into a single loan with one monthly payment, often at a lower interest rate.

Online loan approval platforms provide easy access to such loans by assessing your total outstanding debt and credit profile digitally. Debt consolidation can simplify finances and reduce overall interest costs if done thoughtfully.

Why These Loans Are Ideal for Online Loan Approval

All the above loan types benefit from the online loan approval process primarily because of the speed, convenience, and accessibility it provides. With digital verification and automated credit checks, lenders can approve loans faster, sometimes instantly, while borrowers save time and effort.

Additionally, the online loan approval process often provides borrowers with better control and transparency over loan terms, interest rates, and repayment schedules by allowing easy comparisons across different lenders and products.

Things to Keep in Mind When Choosing a Loan Type Online

- Understand the purpose: Choose the loan that best matches your financial need — don’t use a payday loan to finance long-term expenses.

- Review terms carefully: Online loans might have varying interest rates, fees, and repayment tenures, so read the fine print.

- Assess affordability: Ensure you can meet monthly payments comfortably within your budget.

- Check lender credibility: Only apply through trusted, verified platforms to avoid scams.

Understanding the wide array of loan products available through online loan approval empowers you to select the most suitable option for your financial goals. In the next section, we’ll explore the key advantages of opting for online loan approval over traditional borrowing methods.

The Technology Behind Online Loan Approval

Several technological advancements have enabled the rise of online loan approval:

- Digital Identity Verification: Tools like biometric authentication, facial recognition, and e-KYC (electronic Know Your Customer) processes help verify borrower identities securely.

- Automated Credit Scoring: Algorithms analyze credit bureau data, payment history, and financial behavior to generate a credit score or risk profile.

- Machine Learning and AI: These technologies assess loan applications by detecting patterns and predicting default risks more effectively than traditional manual checks.

- Secure Data Transmission: Encryption and secure servers protect sensitive borrower information during the application process.

Who Can Benefit from Online Loan Approval?

Online loan approval caters to a broad spectrum of borrowers, including:

- Individuals who want quick access to funds without visiting a bank.

- People who prefer digital-first experiences and are comfortable with technology.

- Borrowers in remote or underserved areas with limited bank branch access.

- Applicants needing emergency funds with fast disbursal.

- Young professionals or first-time borrowers seeking convenience.

What Makes Online Loan Approval Different?

The key differentiators between online and traditional loan approval are speed, convenience, and accessibility. While traditional loans can take days or weeks to approve due to manual processes and paperwork, online loan approval systems leverage automation to reduce the approval time to minutes or hours.

Additionally, online platforms often provide greater transparency by allowing borrowers to track application status in real-time, compare loan offers, and understand repayment terms clearly before committing.

Common Myths About Online Loan Approval

Despite its popularity, some misconceptions persist:

- Myth: Online loans are only for small amounts.

Fact: Many online lenders offer loans ranging from a few hundred dollars to large sums for homes or businesses. - Myth: Online loan approval is always instant.

Fact: While many loans are approved quickly, some applications may require manual verification, especially for large amounts or complex cases. - Myth: Online loan approval isn’t secure.

Fact: Reputable lenders use advanced encryption and comply with data protection laws to secure your information.

Understanding the basics of online loan approval helps you appreciate its convenience and decide whether it suits your financial needs. In the next sections, we will explore the advantages and disadvantages of this modern lending approach and help you evaluate if it is the right choice for you.

Advantages of Online Loan Approval

Speed and Convenience

One of the biggest benefits of online loan approval is speed. Many platforms offer instant or same-day approval, which is a lifesaver for emergencies. There’s no need to visit a branch or wait in queues.

Accessibility

Online platforms allow anyone with an internet connection to apply for a loan, removing geographical barriers and making credit accessible even to people in remote locations.

Transparency

Many online lenders provide clear information on interest rates, fees, and repayment terms upfront, so borrowers can make informed decisions.

Flexible Documentation

Online loan approval often requires minimal paperwork compared to traditional loans, reducing hassle and speeding up processing.

Potential Drawbacks of Online Loan Approval

Higher Interest Rates

Due to the convenience and speed, some online loans may come with higher interest rates compared to traditional bank loans, especially if the lender is a non-bank financial institution.

Risk of Scams

With so many online lending platforms, there’s a risk of falling prey to fraudulent websites or predatory lenders. It’s crucial to verify the legitimacy of the lender.

Limited Personal Interaction

Some borrowers prefer face-to-face interaction to clarify doubts or negotiate terms, which online platforms lack.

Credit Risk

Automated systems might reject applicants who have thin credit files or irregular income, where a human loan officer might have been more flexible.

Who Should Consider Online Loan Approval?

Emergency Borrowers

If you need quick funds for emergencies like medical bills, urgent repairs, or unexpected expenses, online loan approval is ideal due to its speed.

Tech-Savvy Individuals

If you’re comfortable with digital platforms and online banking, online loan approval offers a seamless experience.

People Without Easy Access to Banks

Those living in rural or remote areas with limited bank branches benefit greatly from online loan approval.

Who Might Need to Think Twice?

Those With Poor Credit Scores

Online loan algorithms are strict about creditworthiness. People with poor or no credit history might find it hard to get approval.

People Who Need Personalized Support

If you want detailed financial advice or customized loan products, traditional banks may serve you better.

People Concerned About Online Security

If you’re wary of sharing sensitive personal and financial information online, you may prefer offline channels.

Factors to Consider Before Applying for Online Loan Approval

Interest Rates and Fees

Always compare interest rates and hidden fees across lenders. Online loan approval might appear convenient, but costs can add up.

Loan Amount and Tenure

Make sure the loan amount and repayment period fit your financial situation and ability to repay.

Lender Reputation

Research the lender’s reviews, licensing, and customer service responsiveness to avoid scams.

Data Privacy and Security

Check the platform’s privacy policy and data encryption standards to safeguard your information.

Eligibility Criteria

Ensure you meet the eligibility criteria like minimum income, age, and credit score before applying to avoid rejections.

Step-by-Step Guide to Online Loan Approval

- Research Lenders: Identify credible online lenders or fintech companies.

- Check Eligibility: Review minimum income, credit score, and document requirements.

- Gather Documents: Prepare digital copies of ID, income proof, bank statements.

- Apply Online: Fill out the loan application form carefully.

- Wait for Approval: Most lenders use automated systems and give instant decisions.

- Review Terms: Read loan agreements and repayment schedules carefully.

- Accept Loan Offer: Once satisfied, accept the terms and receive funds.

- Repay on Time: Maintain timely repayments to build credit and avoid penalties.

Common Myths About Online Loan Approval

- Myth: Online loans are always expensive.

Reality: While some online loans have higher rates, many platforms offer competitive rates due to lower overhead costs. - Myth: Only people with perfect credit get approved.

Reality: Some online lenders specialize in loans for people with average or low credit. - Myth: Online loans are unsafe.

Reality: Reputable online lenders use advanced encryption and follow regulatory guidelines to protect borrowers.

Also Read :Are Fast Loans Safe or Risky?

Conclusion

Online loan approval is a revolutionary development in personal finance, offering speed, convenience, and accessibility to borrowers worldwide. However, it is not a one-size-fits-all solution. Whether online loan approval is right for you depends on your financial situation, credit profile, urgency of funds, and comfort with digital platforms.

If you value quick disbursal, minimal paperwork, and easy access, online loan approval could be your best bet. On the other hand, if you need personalized advice or have concerns about security, a traditional loan might suit you better.

Before applying, thoroughly research lenders, understand loan terms, and assess your repayment capacity to make an informed decision.

FAQs

What is online loan approval?

Online loan approval is the process where loan applications are submitted and approved digitally via internet platforms, without visiting physical branches.

How fast can I get approved for a loan online?

Many platforms offer instant approval within minutes or a few hours, depending on your eligibility and document verification.

Is online loan approval safe?

Yes, if you use reputable lenders who follow data protection laws and encryption protocols.

What documents do I need for online loan approval?

Typically, a government-issued ID, proof of income, bank statements, and sometimes address proof.

Can I get a loan online with bad credit?

Some lenders offer loans to people with poor credit but expect higher interest rates or collateral requirements.

Are interest rates higher for online loans?

Interest rates vary widely. Some online loans have competitive rates, while others charge more due to convenience and risk factors.

What happens if I miss a repayment on an online loan?

You may incur late fees, impact your credit score, and face potential legal action depending on the lender’s policies.